2025 State of Insurance Report

A Note from the CEO

If there�s one thing we can all agree on, it�s that 2025 hasn�t given us much time to catch our breath. Between shifting regulations, emerging fraud trends, and the nonstop march of AI innovation, the insurance landscape continues to evolve at an unprecedented pace. What used to take years now happens in months � or days, or faster. Staying informed isn�t just helpful anymore, it�s essential.

**At the center of this acceleration is one clear truth: data is everywhere, and intelligence is what you do with it.

From real-time claim analysis to predictive fraud detection, artificial intelligence is no longer a buzzword, it�s a business tool, and increasingly, a competitive advantage. But AI doesn�t work in a vacuum. The real value emerges when it�s combined with experience, ethics, and a deep understanding of the human element in every claim. That�s why publications like this matter more than ever. Whether you�re a carrier, a law firm, or a service provider, we�re all navigating the same waters�and the more we share insights, the stronger our entire industry becomes. In these pages, you�ll find not only trends and data points, but also the questions we should all be asking next. How do we build trust in an increasingly distrustful environment? What does a successful tech-enabled claim investigation really look like? Where does human judgment matter most? And how do we keep building relationships in a world that�s increasingly automated? Our company remains committed to leading with both innovation and integrity. We believe the future of claims is faster, smarter, and more connected, but also more collaborative. As we look ahead, let�s keep challenging old assumptions, exploring new tools, and most importantly, learning from each other.

Thanks for reading, and for being part of this evolving story.

Micah Smith�

Chief Executive Officer

Ethos

Executive Summary

This�report offers a pulse check on the insurance and claims�landscape�in 2025,�highlighting the key trends�shaping fraud, technology, regulation, and consumer trust.�To�ground�our findings,�we surveyed�key�industry�leaders�and gathered insights�from field investigations,�emerging�regulatory developments, and firsthand accounts from claims professionals navigating today�s challenges.��

While the pressures on insurers are not new, the pace and complexity of change have intensified. AI is no longer a siloed initiative;�it�s�embedded across�nearly every�aspect of operations, from fraud detection to�underwriting to�claims automation. Carriers are not just�adopting new�tools but also�rethinking how they work.��

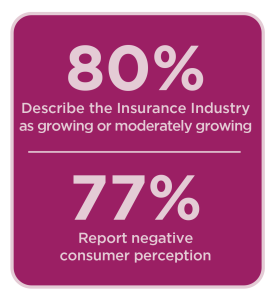

Our survey data underscores this urgency.�Nearly�80%�of respondents�describe the industry as�growing or�moderately growing,�yet�77%�report increasingly negative consumer�perceptions. The disconnect is�largely driven�by rising premiums,�inconsistent�claims�experiences, and growing concerns around�automation.�

Insurers are also contending with surging claims costs, more sophisticated fraud schemes, and the cumulative pressure of climate volatility, regulatory reform, and economic strain.�It�s�not just the pace of change�it�s�the collision of multiple forces at once. For many carriers, the�challenge�lies in responding to these shifts without losing operational focus or customer trust.��

Technology�remains�a cornerstone of industry strategy. Over 93% of respondents�identify�AI as either crucial or important to the industry�s future, with underwriting and claims flagged�as�the�most�likely�areas�to�undergo�significant�transformation. Many are moving beyond pilots and embracing full-scale system upgrades to improve speed, accuracy, and coordination.�

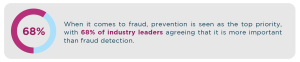

When it comes to fraud, prevention is now�the�priority.�68%�of industry leaders say�they�re�prioritizing�prevention over detection,�investing more heavily in front-end tools and integrated investigative approaches, especially for�high-exposure areas like�complex medical claims�and staged losses.��

Beyond 2025, several shifts are already on the horizon. New CMS audits and health equity mandates will increase compliance risk. The phaseout of federal climate data is accelerating reliance on private modeling. And digital-first insurers are using automation and data�at�scale to outpace slower-moving competitors.�Even midmarket and legacy carriers are reevaluating partnerships, platforms, and workflows to stay competitive.��

What�emerges�is a picture of an industry in motion, modernizing fast, managing uncertainty, and recalibrating how it earns and keeps consumer trust.��

Public Trust and Consumer Attitudes: What it Means for Insurers

While insurance leaders�grow more�confident in advanced fraud tools, consumer trust is slipping.�This disconnect highlights a critical challenge: innovation alone�won�t�bridge the gap if transparency and communication�don�t�keep�pace. As fraud prevention becomes more sophisticated behind the scenes, the industry must work just as hard to build clarity and confidence on the front lines with policyholders.�

Nearly 80% of respondents believe the insurance industry is experiencing moderate to strong growth. Conversely, 77% say consumer attitudes have become increasingly negative over the past three years.****�**Despite�this�logic gap,�most believe their organizations are well-positioned to capture younger policyholders,�particularly�the 26-40 age group.��

The insurance sector is undergoing a transformation that is�largely invisible�to the average consumer. Behind the scenes, carriers are investing heavily in digital infrastructure, AI, and automation to streamline processes, reduce fraud, and enhance underwriting precision. These efforts are driving profitability and operational efficiency, even as public�perception�lags. For younger consumers�who�value transparency�and convenience, these innovations could be�a deciding factor.��

Organizations that communicate value clearly, reduce friction in the claims process, and�demonstrate�ethical use of data will be best positioned to win trust and capture market share in this pivotal demographic.�In short, growth is happening not�in spite of�consumer distrust, but because leading organizations are racing to bridge the gap before it becomes a chasm.�

Why Younger Consumers Remain Skeptical��

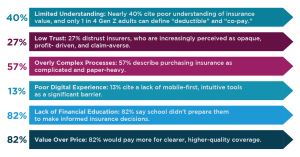

According to a recent GlobalData poll, key barriers for Gen Z and�Millennials�include:��

Our survey�respondents echoed this, with�29%�identifying�improved online tools and platforms as the�greatest�opportunity for better consumer engagement.�

These findings reinforce a deeper challenge: younger consumers�aren�t�rejecting insurance;�they�re�rejecting how it has been delivered.�The issue�isn�t�just low engagement.�It�s�a mismatch between what this generation values and what the industry offers.��

Critically, the disconnect starts early.�Most consumers report never being taught how insurance works.�Without that foundation, even the best-designed apps or pricing models can fall flat.�To close the trust gap, insurers must first close the knowledge gap.�That means going beyond marketing and into education. Imagine tools like �insurance bootcamps� or interactive explainers designed to teach the basics before a policy is even�purchased. Efforts like these, centered on transparency and accessibility, could be key to rebuilding trust and making insurance feel�relevant, ethical, and approachable for a new generation of policyholders.��

The�Impact of Social�Media�and�Public Narratives��

With 84% of Gen Z turning to social platforms�for financial guidance,�public sentiment toward insurers is now largely shaped online.�During open enrollment periods, platforms like X (formerly Twitter) often overflow with�frustration, confusion, and distrust.��

When asked why consumer attitudes have grown more negative,�respondents�cited�rising premiums, poor service, and distrust�stemming�from denied�claims or inconsistent behavior.�A�recurring�theme was a perceived gap between the industry�s operational strategies and consumer expectations,�especially among younger consumers who value speed, personalization, and accountability.�This divide is most visible in high-stakes moments, like denied claims,�where�transparency and fairness matter most.��

These�online narratives�aren�t�just shaping�perception.�They�are�influencing outcomes.�Nuclear verdicts have tripled since 2020**, with the median payout now exceeding $44 million**,�a trend analysts attribute�to�social inflation and�anti-corporate�sentiment�fueled by�viral�mistrust.�The�assassination�of the�UnitedHealth Group CEO�further exposed the fragility of public trust, as�many online users�sympathized with the attacker. In this environment, insurers need to proactively manage their reputations by closely�monitoring�social narratives and carefully aligning their messaging with both legal and strategic priorities.��

Cultural Shifts Fueling Opportunistic Fraud�

Public�attitudes are evolving as quickly as fraud tactics.�**Among 18- to 24-year-olds, only 64% view insurance fraud as a crime, ****compared to 87-96% of older adults. Over a quarter of adults under 35 report feeling motivated to commit fraud, **pointing to�a broader trend�of�rationalized or�even�socially accepted fraud behavior.��

That shift is compounded by growing distrust. Half of insurance customers say they�ve struggled with a claim, and many question whether quotes and payouts are�accurate. As premiums rise and frustration�builds, some policyholders are beginning to�view dishonest claims as justified, especially when those behaviors are normalized by economic pressures or viral narratives online.��

This�erosion of trust�creates a dual challenge:�not only are fraud incidents increasing, but the cultural stigma that once deterred them is fading.�However, technology may offer a path forward.�Nearly half (46%) of U.S. adults say they support the use of AI if it speeds up claims processing, and nearly a third say they would even prefer fully automated providers.��

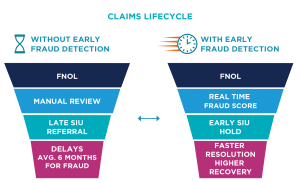

Still, delays tied to fraud remain a major friction point. When vendor engagement or further investigation is triggered late in the process, claims timelines can stretch to six months or more.�The sooner fraud is detected and addressed, the faster claims can be resolved, helping restore consumer confidence and improve�perceptions�of the industry.�

To�meet�this moment, insurers must evolve their approach.�Fighting�fraud�isn�t�just about�detection;�it�s�about understanding the psychology behind it.�Behavioral analytics, early risk indicators, and transparent communication will be key in addressing not just�how�fraud happens,�but�why�it�s�happening,�ultimately�helping�shift the cultural norms that enable it.��

What You Need to Know

The insurance industry is facing a generational trust crisis.�While many organizations see growth opportunities among younger consumers, this same group�often feels disconnected from how insurance is explained or delivered. The gap�isn�t�just digital;�it�s�perceptual, shaped by poor experiences, confusing language, and the viral narratives that define public opinion today.��

As fraud tactics grow more sophisticated and consumer skepticism deepens, insurers must rethink how they build trust from the ground up. That means re-centering the experience around clarity, consistency, and relevance, so insurance feels not only functional, but fair.��

Claims Volumes and Fraud in 2025: What�s Changing and Why it Matters�

Key Trends in Claim and Fraud Activity��

-

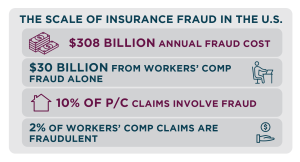

Insurance fraud continues to�exceed $308 billion�annually in the U.S.�(CAIF)

-

Over 10% of P/C claims are suspected�to�involve�fraud.�

-

Staged auto collisions cost an estimated $20 billion annually.�

-

U.S. auto insurance premiums averaged $2,329 in�the first half of�2024, up 15% YoY and 48% from 2021, driven in part by increased fraud exposure and litigation costs.�

-

Fraudulent claims make up 2% of all workers� comp cases, costing approximately $30 billion annually. In New York alone, reported fraud activity rose nearly 30% YoY.��

-

Disability fraud Incidence rates remain under 1%, reflecting strong enforcement under the United States Social Security Administration (SSA) policy.�

In our proprietary survey, insurance professionals�identified�escalating�claims�payouts and�fraud�as the two most significant challenges facing the industry today. This aligns with observed cost trends and the continued evolution of complex fraud schemes. Carriers are feeling�pressure�from both increased claim volumes�and the rising sophistication of fraud, driving demand for faster, smarter claims management tools.��

Notable Developments in Litigation, Subrogation, and Cost Containment��

-

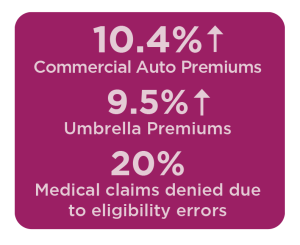

In Q1 2025, commercial auto and umbrella premiums rose 10.4% and 9.5%,�respectively. The Council of Insurance Agents & Brokers (CIAB) attributes part of this increase to third-party litigation funding, which�drives up�settlement costs.�

-

Subrogation continues to recover billions annually. Timely, data-driven investigations now serve as a critical counterbalance to rising loss ratios.�

-

About 20% of medical claims are denied due to eligibility errors. Real-time verification tools�are helping�reduce administrative costs and friction.�

Fraud Prevention in Action: Industry Strategies and Case Response�

As fraud threats grow more complex, leading insurers are moving quickly to embed detection tools and analytics earlier in the�claims�lifecycle. These efforts aim to manage rising claims�volumes while�keeping�up�with increasingly sophisticated schemes.��

Carriers are�now using�real-time AI-driven fraud scoring at First Notice of Loss (FNOL), allowing for faster SIU referrals and fewer false positives.�Some�have�seen strong results from machine-learning models that detect fraud up to three days earlier, enabling 83% more�claims to be processed and improving fraud capture by 20%. In February 2025,�one major�carrier�invested in�a digital ID authentication platform to proactively combat synthetic identity fraud at the point of entry.��

Yet even with these tools in place, organized fraud continues to pose significant challenges. In late 2024,�construction captive insurer�Ionian RE�and its contractors filed a federal RICO lawsuit alleging a coordinated fraud ring involving staged workplace falls. The case revealed suspected collusion�between�claimants, law firms, and medical providers.�A second suit filed in June 2025 expanded the number of parties and the scope of the alleged conspiracy.�

This case, among others, highlights the need for cross-functional coordination within insurers. Legal, SIU, and analytics teams must work in tandem to detect patterns early, respond decisively, and protect against systemic�loss.�Both strategic investment and cross-disciplinary response will be essential to keeping pace with the rapidly evolving fraud landscape.�

What You Need to Know�

Survey data confirms what many in the industry are already experiencing: escalating claims payouts and fraud are the most urgent challenges of 2025. These twin pressures are reshaping claims operations, requiring both early detection and cost containment strategies. Insurers are responding by embedding�tools like�automation�and�fraud analytics at intake to manage�complexity and reduce exposure. As AI-powered�schemes proliferate and legal costs rise,�speed and coordination across investigative, legal, and claims teams are becoming vital. Competitive�advantage�will depend on how well insurers�adapt�their operations in real time.��

**New Tactics in Claims Investigation and Fraud Prevention **�

OSINT and Surveillance Tools��

To keep pace with the increasing complexity of fraud, insurers are adopting open-source intelligence (OSINT) tools, like social media monitoring platforms, geolocation trackers, and facial recognition software. These tools can reduce manual investigation time from 3.5 hours to 15 minutes, enabling small teams to manage thousands of cases annually.��

But tools alone�aren�t�enough. Effective OSINT�use�demands legal precision, investigative fluency, and ongoing training, resources that many carriers struggle to�maintain.�While some build in-house capabilities, many find it more efficient to rely on dedicated external teams with the�expertise�to�operate�these tools�at scale.��

**Speed cannot come at the expense of scrutiny. As carriers modernize, balancing automation with informed oversight will be crucial.

As one SIU director noted,�speed cannot come at the expense of scrutiny. As carriers modernize, balancing automation with informed oversight will be crucial.��

Legal and Privacy Considerations��

New privacy laws are reshaping how insurers collect and use data. In California, SB 354�(effective 2025) requires opt-in consent and stricter data minimization, prompting many carriers to reevaluate their workflows to ensure compliance and�maintain�public trust.��

Texas has also increased enforcement under its new Data Privacy and Security Act (TDPSA), with recent lawsuits targeting unauthorized geolocation tracking. While location data is often used to detect fraud or enhance risk models, collecting it without clear consent or disclosure can lead to legal exposure and reputational harm.�

Despite these challenges, geolocation�remains�a valuable investigative tool when used properly. To reduce risk, insurers should build privacy-by-design into their processes, ensuring informed consent, vetting data partners, and�maintaining�compliance oversight throughout the�claims�workflow.���

Strategic Shift:�From Volume to Value�

The global insurance fraud detection market, valued at $5.37 billion in 2024, is projected to grow to $54.59 billion by 2034,�driven by a 26.1% compound annual growth rate�(CAGR).�

This surge reflects a clear shift from high-volume, manual investigations�toward�more targeted, technology-enabled strategies. As fraud becomes more sophisticated, insurers are moving away from sheer case volume and focusing instead on high-impact cases supported by analytics, AI, and precision surveillance.�

What You Need to Know�

The industry is shifting toward value-focused, technology-driven investigations, recognizing the need to balance volume with impact.�This balance reflects an understanding that successful fraud management�requires both proactive measures to�prevent�fraud before it happens and robust investigative capabilities to catch and mitigate ongoing schemes.�Moving forward, insurers that integrate prevention and detection strategically and�leverage�advanced technology will be best positioned to combat increasingly�complex�fraud.��

Emerging Fraud Types in 2025-26: Evolving Threats and Tactics�**�

Fraud tactics are becoming more sophisticated and harder to detect, driven�largely by�organized operations and advanced technologies.�A growing share�of these schemes are designed to bypass traditional detection systems and�exploit�vulnerabilities before insurers even know they exist.��

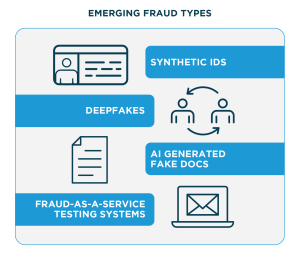

Organized fraud rings now dominate the threat landscape,�**with 71% **of fraud and risk leaders reporting that professional operations�were responsible for�most attacks in 2024. These groups are�leveraging�AI,�deepfake�tools, synthetic identities, and other methods�to execute large-scale, coordinated campaigns.��

Synthetic Identity Claims�

Fraud is�increasingly fueled by AI-driven synthetic identities�fictitious profiles that combine real and fake data to evade detection.�Unlike traditional identity theft, which involves stealing an existing person�s�entire�identity, synthetic identity fraud creates entirely new�individuals�who don�t actually exist.�These identities often�pair�real data, such as a valid Social Security number, with fake names, birthdates, and addresses. Over time, they can build legitimate-looking credit histories, making fraudulent claims appear credible on the surface but difficult to verify.��

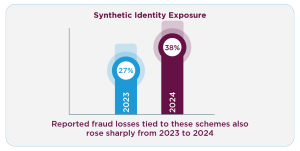

This tactic contributed to an estimated�$3.2 billion�in synthetic identity exposure in the first half of 2024, a 7% year-over-year (YoY) increase. Reported fraud losses tied to these schemes also rose sharply, from 27% in 2023 to 38% in 2024.��

Deepfake-Driven Claims and Testimony�

Deepfake�technology is�emerging�as a new front in insurance fraud, enabling the manipulation of evidence in increasingly convincing ways. Fraudsters are now using AI-generated video, audio, and even virtual interviews to support false injury claims, property damage reports, and fabricated statements.�

**In just the past three years, deepfake-related fraud has surged by over 2,100% and now accounts for one in every 15 financial fraud cases across sectors.

As these tools become more accessible, the risk of manipulated testimony and falsified documentation is rapidly expanding.��

Fraud-as-a-Service (FaaS) and Document Template Attacks�

Fraud-as-a-Service is lowering the barrier to entry for bad actors. Online platforms now offer ready-made fraud kits that include AI-generated identification, forged documents, and spoofed credentials.�Less experienced fraudsters�are�increasingly�using�these tools to launch�sophisticated, coordinated attacks against insurers. In fact, the use of AI-generated identity variants submitted to carriers rose by 33% ****YoY.**�Often, these variants are deployed to quietly test claim intake systems,�probing for�weaknesses before larger-scale fraud campaigns are launched.��

Coordinated Hybrid Claims��

Fraud networks are�now�blending elements of medical, auto, and disability fraud into single, synchronized schemes. These hybrid claims may involve staged accidents, exaggerated injuries, and falsified medical records, often�submitted�across different carriers or departments to avoid detection.��

**By exploiting communication gaps between insurers, providers, and investigators, these schemes appear legitimate in isolation but reveal patterns when viewed holistically.

Because they cross traditional claim lines, hybrid schemes are more difficult to catch with rule-based systems and often require early cross-functional collaboration and data sharing to detect and dismantle.�

What You Need to Know�

The rise of sophisticated, tech-enabled fraud schemes emphasizes the urgency of modernizing fraud detection capabilities and reinforcing digital identity verification at intake. Carriers are increasingly investing in AI-driven screening tools, anomaly detection, biometric verification, and cross-functional investigative collaboration. However, even the most advanced technologies require trained human oversight to assess nuanced risks and interpret complex cases. As these evolving tactics continue, proactive investigative partnerships and faster, secure data sharing across stakeholders will be essential to outpacing fraud and maintaining consumer trust.�

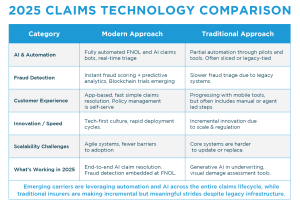

Tech-Driven Transformation in Claims Processing�**�

When asked which areas�are�poised�for the most tech-driven innovation over the next�three to five�years, respondents ranked underwriting highest (34%), followed by claims processing (27%) and customer experience (16%). These results highlight claims as a central focus of digital�transformation, alongside other core operational functions.��

InsurTech�Momentum in 2025��

**Investment in InsurTech surged in the first quarter of 2025, rising 90.2% YoY to�$1.31 billion, with much of the growth driven by AI-focused firms.

Investors are prioritizing technologies that improve claims automation and fraud analytics, signaling strong confidence in AI�s potential to streamline the claims process.��

Speed and transparency in claims handling are increasingly important to consumers, who expect quicker outcomes and clearer communication. By enabling faster claim completion,�InsurTech�innovations have the potential to improve customer satisfaction and help rebuild trust in the industry.�As adoption grows, carriers will need to carefully balance rapid innovation with adherence to evolving regulatory requirements and the realities of integrating new tools within existing operational frameworks.�

Comparative Technology Use: Traditional vs. Non-Traditional Carriers�

Nontraditional carriers�have been faster to implement�emerging�technologies, including automation, real-time fraud analytics, and blockchain-based claims processing. Their digital-first�models and streamlined operations make it easier to integrate and test new�tools at�scale.��

Traditional carriers, on the other hand,�operate�within complex, highly�structured�environments and often rely on legacy systems that have been built over decades. These factors can�slow�the pace of adoption, not due to a lack of innovation, but because changes must be implemented thoughtfully across large, interconnected systems.��

Still, traditional insurers stand to gain significantly from�even gradual modernization. Incorporating newer technologies can improve operational efficiency, accelerate claims processing,�strengthen�fraud detection, and enhance the overall customer experience. As innovation spreads, traditional and nontraditional carriers alike are helping shape the industry�s next chapter.��

Artificial Intelligence in Claims: What�s Working��

AI continues to gain traction across the insurance sector, with 93% of industry survey respondents calling it crucial or important to future growth and innovation.

Still, not all�sentiment is�unanimous. One�respondent noted, �AI is�necessary�only because of its hype,�not�because it is invaluable, essential,�or even good for the marketplace,� reflecting lingering skepticism in some corners of the industry.��

Despite mixed opinions, real-world use cases show strong results. Automation and AI triage tools now enable FNOL, auto-adjudication, and early fraud detection, cutting claim cycle times by 60% and reducing operational�costs�by 20 to�30%�in states like Florida. Natural Language Processing (NLP) and Optical Character Recognition (OCR) further streamline workflows by extracting data from unstructured sources such as medical records and adjuster notes, reducing human�error�and improving accuracy.��

AI has also improved fraud detection outcomes.�In fiscal year 2024, the U.S. Department of the Treasury reported recovering over $4 billion ****using enhanced AI-driven processes.**�These results show that, when thoughtfully deployed, AI can improve operational scalability, streamline claims, and deliver measurable ROI.���

AI Underperformance and Limitations��

While AI is delivering clear operational benefits, its limitations are increasingly�evident. Some systems have produced high denial rates, leading to litigation and reputational risk tied to bias and false positives. AI also struggles with complex or atypical claims that require human judgment, especially high-severity cases where context matters. These constraints�highlight�the need for balanced implementation. Automation should enhance, not replace, human oversight.��

**Automation should enhance, not replace, human oversight.

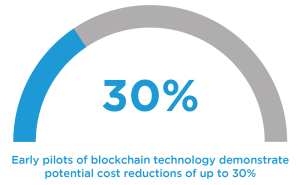

Blockchain: An Emerging Tool in Claims Integrity��

Blockchain technology is proving valuable for enhancing transparency and reducing fraud in claims processing. Smart contracts now enable multi-party validation and create immutable audit trails, which are especially useful in health and parametric insurance claims. Early pilots from companies like Lemonade and Etherisc demonstrate potential cost reductions of up to 30%, along with improved fraud resistance through automated, tamper-proof payment flows. Though still�emerging, blockchain shows strong promise in scenarios requiring speed, integrity, and accountability.��

Top 3 Questions for Claims Leaders in 2025

1. Can our systems support real-time automation?

Are we equipped for digital FNOL, instant triage, and AI-driven fraud scoring or are legacy platforms holding us back?

2. Are we measuring ROI on claims tech beyond just implementation?

Are we tracking actual business impact: faster cycle times, lower cost, fraud reduction?

3. Are frontline teams prepared to work with AI tools?

Do adjusters, SIU, and analysts have digital fluency to trust and leverage automation effectively?

What You Need to Know�

Technology is reshaping claims today���not�as a distant goal, but as a critical advantage. Automation and AI already boost efficiency, accuracy, and fraud detection. Yet uneven adoption is widening the�gap�between digitally advanced carriers and those�working through legacy�systems.�The challenge�isn�t�whether to modernize, but how to do so with care and precision, balancing speed, cost, and scale to keep pace in a competitive landscape.�

Medical Management in�Flux: Regulatory and Process Shifts**�

Integrated Medical and Claims Strategies�

An insurer�s ability to control costs and improve outcomes is often constrained when medical management and claims functions�operate�separately.�Coordinated oversight that combines clinical review, claims management, and fraud detection delivers measurable savings and better results.��

For example, a major U.S. property and casualty insurer integrated 25 years of claims and clinical data through P&C Global, achieving $115 million in annual savings and�identifying�$415 million in�additional�cost-reduction opportunities.

**Supporting this approach,�a 2024 meta-analysis found that combining clinical oversight with process controls reduced costs by 5.6% and improved outcomes by 6.2%.

Given these findings, aligning medical review closely with fraud detection and claims workflows is no longer optional for insurers seeking�a�competitive advantage; it�serves as a critical performance multiplier that drives both operational efficiency and improved claims�outcomes.��

Navigating a Changing CMS Landscape�

As CMS expands its�regulatory�reach�in 2025 and beyond, insurers face a growing array of compliance challenges that�impact�claims, billing, care management, and documentation.�Heightened audit activity,�new reporting mandates,�and care coordination reforms�are reshaping expectations across the board.�Meeting these demands will require not just more resilient systems, but also a shift in how teams coordinate and respond to change as new policies take shape.�The following regulatory developments�illustrate the scale and urgency of�such�changes:�

-

**Audit Expansion and Recoupment Risk: **CMS is significantly increasing its oversight in 2025, with annual Medicare Advantage contract audits rising from 60 to 550. The Risk Adjustment Data Validation (RADV) final rule no�longer�permits�extrapolation of audit findings,�substantially raising�recoupment�risk�for insurers. To mitigate this exposure, carriers must strengthen documentation standards and implement thorough pre-audit internal reviews.��

-

**Utilization Reporting Requirements: **Alongside expanded audits,�utilization�reporting demands have intensified. Detailed Medicare Advantage�utilization�data was due to CMS by January 31, 2025, requiring strict formatting and audit readiness. This increases operational burdens on claims and audit teams, making infrastructure upgrades and enhanced workflow controls�critical.��

-

**Billing, Fee Schedule, and Case Management Updates: **CMS is phasing in Graduate Medical Education (GME) adjustments through 2027, which may increase audit complexity for academic hospital claims. The 2025 Physician Fee Schedule updates bring new billing rules and adjusted Part B rates, affecting provider compensation and claims valuation. Additionally, care management enhancements, including expanded caregiver support, telehealth billing, and preventive services, are reshaping claims coordination and processing. Claims professionals must adapt quickly to these evolving codes and documentation requirements to maintain compliance and optimize outcomes. �

-

**Prior Authorization Reform and Health Equity Tracking: **Effective 2026, the CMS Prior Authorization Reform introduces digitization and timeline mandates requiring technology upgrades beginning now.�Health equity tracking rules�also�require�Medicare Advantage plans to notify non-users of supplemental benefits annually by June 30. These regulations add complexity around�outreach, care planning, and benefit engagement,�requiring increased operational agility and stronger compliance programs.��

What You Need to Know�

Rising medical complexity and regulatory pressure are pushing insurers to move beyond siloed operations. When clinical review, claims processing, and fraud detection function in isolation, opportunities for efficiency and impact are lost.��

At the same time,�CMS�is introducing rules�that touch�nearly every�part of the�claims�lifecycle. New mandates are tightening�expectations around documentation and reshaping how plans approach care oversight.�Maintaining�competitiveness�will�require�updated infrastructure and a more seamless connection between documentation and clinical insight.�This shift�won�t�happen overnight, as changes demand both strategic investment and day-to-day execution. But the direction is clear: the future of claims performance lies in�integration, not compartmentalization.��

2025 Regulation: What�s New and Who�is�Affected�**�

Regulatory developments at the federal, state, and environmental levels are creating a more complex and fragmented oversight landscape. The following flashpoints outline key areas of emerging risk and operational impact�that may require increased attention in the months ahead.��

Federal Oversight Shifts Under Executive Order 14215�

Executive Order 14215 expands presidential authority over independent federal agencies such as the Consumer Financial Protection Bureau (CFPB) and�the�Federal Trade Commission (FTC), enabling faster regulatory changes across industries including insurance, healthcare, and consumer protection.

One result is a 50% reduction in CFPB supervisory exams, paired with a sharper focus on targeted fraud investigations, particularly involving military personnel and vulnerable populations. While routine oversight may decrease, insurers face greater risk of focused enforcement actions triggered by deceptive denial patterns and consumer complaints.��

NOAA Data Disruption and Climate Risk Preparedness��

In 2025,�NOAA halted updates to its Billion-Dollar Disaster Database�for the first time in 45 years,�pausing�a key federal resource for tracking catastrophe losses.�This, along with staffing reductions at NOAA and FEMA, has added new complexity to how insurers evaluate and plan for seasonal risk.��

In response, many carriers are shifting to private climate risk platforms and third-party catastrophe models. While these offer speed and customization, they differ in accuracy and approach, requiring stronger internal vetting. Insurers must�adapt by building more flexible modeling strategies and�identifying�trusted sources that can fill�the�gaps left by federal delays.

**The shift also calls for clearer planning around disaster exposure�as traditional public resources become less reliable.��

State-Level Regulatory Momentum and Cyber-Fraud Oversight��

The NAIC�s 2025 Roadmap, titled �Security Tomorrow,� emphasizes strengthening state-based regulation, including more localized eligibility rules and enhanced fraud oversight. As a result, carriers should anticipate greater variation across states in consumer protection laws, claims standards, and market conduct expectations. Additionally, the Financial Industry Regulatory Authority�s (FINRA) 2025 Overnight Report urges�increased scrutiny of cyber-enabled fraud,�particularly�schemes using generative AI to create false identities and digital claims.��

These trends�mean insurers must invest in compliance agility to keep pace with shifting state regulations, while also expanding cybersecurity measures and digital fraud detection capabilities to meet evolving enforcement demands.��

What You Need to Know�

While�regulatory change ranked�low among immediate concerns in our survey,�external signals suggest it�won�t�stay that way. Federal oversight is narrowing�in�scope,�state-level�mandates�are diverging,�and climate�volatility continues to pressure reinsurance and preparedness strategies.�The�loss of consistent federal disaster data only adds to this�uncertainty.��

As 2026 approaches, insurers may need to rethink how they�monitor�regulatory trends and respond to risk in a more decentralized environment.�This could mean investing in more localized data collection,�strengthening�state-level�compliance capabilities, or adopting flexible underwriting models that account for shifting environmental baselines.�

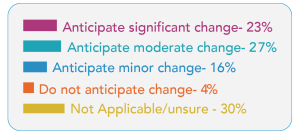

How�Insurers Are Responding to Emerging Risks�**�

Amid�mounting risk�volatility,�including climate�change�and evolving pressures,�a majority of�insurers�anticipate�changes to�coverage availability or premiums;�only 4.5% of survey respondents expect no adjustments.�This widespread expectation aligns with environmental risks ranking as one of the top three challenges facing�the industry. As insurers raise rates and reduce access in high-risk areas, they face growing consumer dissatisfaction.�Transparent, meaningful education around these issues is essential�if the industry wants to shift public�perception�in a positive direction.�

Generative AI and Advanced Risk Modeling�

To manage increasing volatility and strengthen risk forecasting, insurers are rapidly adopting generative AI, with 76% of U.S.�carriers�using it in at least one business function. This technology enables the simulation of thousands of risk scenarios, improving preparedness for emerging threats and market�uncertainty.��

Claims and underwriting teams are aligning processes with AI-driven forecasting models to enhance risk assessment and pricing accuracy. At the same time, carriers are integrating predictive analytics and IoT-enabled real-time risk monitoring, allowing for proactive alerts, loss mitigation, and better customer retention. These advances require�claims�professionals to adapt to evolving risk profiles and incorporate dynamic data into investigations.�

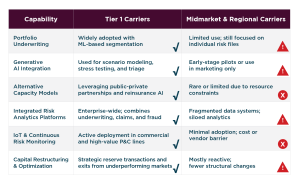

Underwriting Innovation and Capital Flexibility��

Underwriting is�emerging�as the top area for technology-driven innovation over the next three to five years, with a clear shift toward portfolio-level risk analysis, AI modeling, and more flexible capital strategies.�In 2025-26, insurers have embraced alternative capacity models, including AI platforms and public-private partnerships, to diversify risk and access new sources of capital.��

Instead of focusing solely on individual policies, portfolio underwriting uses machine learning to assess and manage risk across entire�books of�business dynamically. To stay competitive and resilient, underwriters need to strengthen their analytics skills and adopt a broader, portfolio-focused approach to capital management.��

**Tier 1 carriers are redefining�underwriting with�enterprise-scale AI, integrated data, and capital flexibility. Midmarket players risk falling behind unless they focus on modular innovation and modernizing their data systems.�

Strategic�Industry�Moves��

Leading insurers are making significant strategic moves to complement technological progress. One major data analytics vendor secured a $1.3 billion investment to reduce leverage and expand its tech-driven distribution capabilities. A leading global insurance organization improved data accuracy from 75% to over 90% by applying generative AI to its underwriting workflows, resulting in faster processing and more precise pricing. Another global insurer realigned its portfolio by closing underperforming segments, transferring $1.6 billion in reserves, and achieving growth in premiums�as well as�improved profitability.��

These actions�demonstrate�how top carriers balance innovation with disciplined capital and portfolio management to strengthen�their�market position and resilience.��

What You Need to Know�

The industry is investing heavily in AI, analytics, and capital flexibility,�with underwriting identified as the leading area for tech-driven innovation.�As insurers navigate mounting claim costs, fraud exposure, and climate-related disruptions,�it�s�clear that innovation must be grounded in real-world risk. Aligning technology initiatives with core operational pressures will be critical.�Forward-looking strategies should�strike a�balance�between advancing capabilities and managing the financial and environmental�unpredictability�reshaping the industry.���

Why Investigative Services Still Matter**�

Adapting to New Threats in 2025�

The complexity of claims continues to grow, driven in part by cyber incidents and natural disasters. Investigative services are evolving to meet these challenges with a more proactive stance. Artificial intelligence and machine learning now enable early fraud detection, often within just two weeks of claim submission. Forensic consultants are shifting�their focus from reactive investigations to�identifying�vulnerabilities and�advising on�prevention strategies. These advancements not only improve the accuracy of complex claim assessments but also enhance customer satisfaction and contribute to reducing future claim volumes.��

Despite�rapid�breakthroughs in technology, traditional investigative services�remain�a vital�component�in combating insurance fraud. Independent fieldwork, such as onsite inspections and claimant interviews, uncovers deceptive activity that automated systems alone may miss. By blending human�expertise�with technological tools, insurers are better equipped to detect complex fraud schemes, protecting�resources�and honest policyholders alike by reducing false claims.�

Technology in Action: Real-World Investigative Tools��

Insurers are�leveraging�a variety of advanced tools and industry collaboration to sharpen fraud detection capabilities: social media analysis uncovers inconsistencies between reported claims and claimants��online behavior,�and�shared fraud databases strengthen collective efforts to�identify�repeat offenders.�Organizations like the Coalition Against Insurance Fraud, which�comprises�over 300 members,�play a critical role in promoting legislation, education, and coordination across insurers.�Such�efforts highlight the indispensable role of investigative services in an increasingly sophisticated fraud landscape.��

Supporting Regulatory Compliance and Legal Defense�

Investigative services also play a crucial role in meeting regulatory requirements and supporting legal processes. Detailed fieldwork and thorough documentation provide essential evidence for audit responses,�claims�disputes, and litigation defense. By ensuring investigations are compliant with evolving legal standards, insurers reduce regulatory risk and strengthen their position in both internal reviews and external proceedings.�These evolving investigative approaches position insurers to detect fraud earlier, prevent losses, and strengthen overall�claims�integrity.��

What You Need to Know�

In today�s evolving fraud landscape, the value of investigative services lies not just in uncovering fraud, but in shaping smarter prevention strategies. As carriers face more complex claims and rising digital threats, the most effective fraud defenses combine cross-carrier collaboration, shared intelligence platforms, and adaptable field�expertise. Looking ahead,�the ability to integrate investigative insight into broader risk and claims strategies will be critical for�maintaining�both efficiency and policyholder trust.��

Key Takeaways�

The 2025 insurance landscape�is defined by rapid technological change, evolving fraud tactics, and increasing regulatory demands. Success will depend on carriers� ability to integrate innovative tools, adopt proactive investigative approaches, and�strengthen�collaboration�across the ecosystem to navigate emerging risks and meet rising consumer expectations.��

2025�Key�Trends�

-

The rapid adoption of AI and automation in claims and underwriting�is�enhancing�efficiency, accuracy,�and early fraud detection.�

-

Fraud schemes are becoming more sophisticated,�with�the rise of synthetic identities and AI-enabled tactics�necessitating�modernized controls and proactive monitoring.��

-

Regulatory complexity�is intensifying, with narrowing federal oversight and heightened scrutiny at the state level.�

-

Integrating medical management within claims workflows�is yielding�measurable cost savings and improved claimant outcomes.��

Looking�Ahead:�Emerging 2026 Developments��

-

Expanded CMS audits and�new�health equity mandates will increase compliance�pressures for insurers and investigative partners.��

-

The withdrawal of federal climate data is accelerating a shift toward private and in-house risk modeling solutions.��

-

Generative AI�adoption will expand across underwriting and fraud analytics, underscoring the need for robust human oversight and ethical governance.�

Competitive Landscape: Traditional vs. Non-Traditional Players��

-

Nontraditional�carriers are advancing quickly in digital innovation and fraud analytics, gaining a competitive edge through scale and adaptability.��

-

Traditional and midmarket insurers�may�risk falling behind without accelerated modernization of legacy systems and investigative infrastructure.��

Challenges and Opportunities�for Insurers and Investigative Partners��

-

The rise in complex hybrid fraud and medical claims calls for earlier, integrated investigative strategies.��

-

Pressure for faster, more transparent claims experiences is increasing demand for real-time analytics and cross-functional coordination.��

-

Enhanced collaboration and secure data sharing between carriers and investigative partners will be crucial in combating organized fraud.��

-

Balancing�automation with human�expertise�remains�essential to ensure fairness, accuracy, and regulatory alignment.�

About Ethos

Ethos is a full-service claims investigation and medical management fi rm headquartered in St. Petersburg, Florida. Ethos provides comprehensive fraud prevention, investigation, and medical claims management solutions to insurance companies, self-insured employers, attorneys, and third-party administrators. Since 2006, the company has delivered nationwide and international coverage, serving all 50 states and more than 75 countries. Our vision is to deliver better data for better decisions, empowering our clients with the insights they need to achieve optimal outcomes. We combine deep investigative expertise with advanced technology to remain one of the most tech-enabled, customer-centric claims services companies in the industry. For more information, visit ethosrisk.com or contact marketing@ethosrisk.com

�

Sources:

2025�FINRA Annual Regulatory Oversight Report. FINRA. (2025, January).�https://www.finra.org/sites/default/files/2025-01/2025-annual-regulatory-oversight-report.pdf�

Adams, S. (2024, August 21).�The ROI of Automated OSINT, Part I: Insurance Fraud & Claims Investigations.�Skopenow.�https://www.skopenow.com/news/roi-of-osint-part-i-insurance�

Alloy. (2025, January 28).�Majority of Bank Fraud Committed by Professional Fraud Rings, New Report Finds.�PR�Newswire.�https://www.prnewswire.com/news-releases/majority-of-bank-fraud-committed-by-professional-fraud-rings-new-report-finds-302361827.html�

Amacher, E. (2024, June 3).�Nuclear Verdicts Surge to $14.5 Billion in 2023, Report Shows.�Insurance�Journal.�https://www.insurancejournal.com/magazines/mag-features/2024/06/03/777420.htm�

Antoniuk, S. (2025, June 17).�Blockchain in�Insurance: Ensuring Data Security and Fraud Prevention Examples.�Litslink.�https://litslink.com/blog/blockchain-in-insurance-ensuring-data-security-and-fraud-prevention-examples�

Araullo, K. (2025, May 19).�Third-party litigation finance linked to rising insurance premiums. Insurance Business America.�https://www.insurancebusinessmag.com/us/news/regulatory/thirdparty-litigation-finance-linked-to-rising-insurance-premiums�ciab-536185.aspx�

Ashare, M. (2024, November 6).�AIG leans on generative AI to speed underwriting.�CIO Dive.�https://www.ciodive.com/news/aig-insurance-agentic-generative-ai-underwriting/732183/�

Attor�ney Gen�er�al Ken Pax�ton Sues All�state and Ari�ty for Unlaw�ful�ly Col�lect�ing, Using, and Sell�ing Over 45 Mil�lion Amer�i�cans� Dri�ving Data to Insur�ance Companies. Ken Paxton Attorney General of Texas. (2025, January 13).�https://www.texasattorneygeneral.gov/news/releases/attorney-general-ken-paxton-sues-allstate-and-arity-unlawfully-collecting-using-and-selling-over-45�

Birch, D. (2025).�The Battle Against AI-driven Identity Fraud.�Signicat.�https://www.signicat.com/the-battle-against-ai-driven-identity-fraud�

Carlyle�investment boosts insurance�brokerage�Trucordia�s�valuation to $5.7 billion.�Reuters. (2025, June 4).�https://www.reuters.com/business/insurance-brokerage-trucordia-valued-57-billion-after-carlyles-strategic-2025-06-04/�

Elad, B. (2024, February 13).�Social Security Fraud Statistics 2024 By Facts,�Trend�and Insights. Enterprise Apps Today.�https://www.enterpriseappstoday.com/stats/social-security-fraud-statistics.html�

Fraud�Industry Benchmarking Resource. (2025, June 30).�Q2 2025 Digital Trust index: AI Fraud Data and insights. Sift.�https://sift.com/index-reports-ai-fraud-q2-2025/�

FTC. (2025, March 10).�New FTC Data Show a Big Jump in Reported Losses to Fraud to $12.5 Billion in 2024. Federal Trade Commission.�https://www.ftc.gov/news-events/news/press-releases/2025/03/new-ftc-data-show-big-jump-reported-losses-fraud-125-billion-2024�

Genpact. (2025, April 29).�Genpact�Study Shows Insurance Customers Embrace AI When Value and Benefits Are Clearly Demonstrated.�PR�Newswire.�https://www.prnewswire.com/news-releases/genpact-study-shows-insurance-customers-embrace-ai-when-value-and-benefits-are-clearly-demonstrated-302440905.html�

Global�InsurTech�Report for Q1 2025. Gallagher Re. (2025, May 7).�https://www.ajg.com/gallagherre/news-and-insights/global-insurtech-report-q1-2025/�

GlobalDataFinancialServices. (2025, June 9).�Rebuilding trust and simplifying insurance will win over the next generation. Life Insurance International.�https://www.lifeinsuranceinternational.com/analyst-comment/trust-simplifying-insurance-next-generation/�

Henney, M. (2024, August 28).�Car insurance premiums could skyrocket 50% in some states this year. Fox Business.�https://www.foxbusiness.com/economy/car-insurance-premiums-could-skyrocket-50-some-states-year�

Insurance�Fraud Detection Market Size Analysis � Market Share, Forecast Trends and Outlook Report (2025-2034).�Claight�Corporation (Expert Market Research). (2024, November 12).�https://www.expertmarketresearch.com/reports/insurance-fraud-detection-market�

Jackman, S., Silverman, J., Willis, C., & Sommerfield, L. (2025, April 17).�CFPB Announces 2025 Supervision and Enforcement Priorities. Troutman Pepper Locke.�https://www.consumerfinancialserviceslawmonitor.com/2025/04/cfpb-announces-2025-supervision-and-enforcement-priorities/�

Jackson-Matsushima, L. (2025, January 16).�150+ Workers Compensation Statistics.�Insuranceopedia.�https://www.insuranceopedia.com/workers-compensation-statistics�

Law, M. (2024, October 23).�Deloitte: Insurers Race to Deploy AI Amid Profit Pressures.�InsurTech�Digital.�https://insurtechdigital.com/articles/deloitte-insurers-race-to-deploy-ai-amid-profit-pressures�

McConvey, J. R. (2025, May 21).�Au10tix�identifies�new�deepfake�fraud�tactic�that�probes for�security vulnerabilities.�BiometricUpdate.com.�https://www.biometricupdate.com/202505/au10tix-identifies-new-deepfake-fraud-tactic-that-probes-for-security-vulnerabilities�

NAIC�Announces 2025 Initiatives. NAIC. (2025, February 14).�https://content.naic.org/article/naic-announces-2025-initiatives�

NAIC. (2024, July 22).�Only About 1 in 4 Gen Z Adults Can Define �Deductible� and �Co-Pay.��NAIC.�https://content.naic.org/article/only-about-1-4-gen-z-adults-can-define-deductible-and-co-pay�

New�York State. (2025, April 15).�NYS Inspector General Releases 2024 Workers� Compensation Fraud Report. Offices of the Inspector General.�https://ig.ny.gov/news/nys-inspector-general-releases-2024-workers-compensation-fraud-report�

O�Neill, S.,�Schwedel, A., Jones, D., & Brettel, T. (2025, March 31).�Bridging the Protection Gap: Affordability, Access, and Risk Prevention. Bain & Company.�https://www.bain.com/insights/bridging-the-protection-gap-in-insurance�

Product�Team. (2025, March 6).�Real-Time Insurance Eligibility Verification: How Healthcare Providers Can Maximize Revenue & Efficiency in�2025.�CERTIFY Health.�https://www.certifyhealth.com/blog/real-time-insurance-eligibility-verification�

Rocks, S., Berntson, D., Gil-Salmer�n, A., Kadu, M., Ehrenberg, N., Stein, V., &�Tsiachristas, A. (2020).�Cost and effects of integrated care: a systematic literature review and meta-analysis.�Eur�J Health Econ.�https://pmc.ncbi.nlm.nih.gov/articles/PMC7561551/#:~:text=Although%20indicating%20a,with%20integrated%20care.�

Rodriguez, C. (2025, January 30).�Claims Management: When and How to Engage Vendors. Ethos Risk.�https://ethosrisk.com/blog/claims-management-when-and-how-to-engage-vendors/�

Schneider, P. (2025, May 29).�Insurance Claims Automation: 10 Powerful Benefits in 2025. Schneider and Associates Insurance.�https://schneider-insurance.com/insurance-claims-automation/�

Stengel, J. (2025, April 30).�The cost of deception: Navigating the challenges of staged auto accidents.�AXA XL.�https://axaxl.com/fast-fast-forward/articles/the-cost-of-deception�

Sumsub. (2025, June 12).�Synthetic Identity Document Fraud Surges 300% in the U.S. ��Sumsub�Warns E-Commerce,�Healthtech�and Fintech at Risk.�https://sumsub.com/newsroom/synthetic-identity-document-fraud-surges-300-in-the-u-s-sumsub-warns-e-commerce-healthtech-and-fintech-at-risk/�

Treasury�Announces Enhanced Fraud Detection Processes, Including Machine Learning AI, Prevented and Recovered Over $4 Billion in Fiscal Year 2024. U.S. Department of the Treasury. (2024, October 17).�https://home.treasury.gov/news/press-releases/jy2650�

U.S. Health Insurer Uses Analytics to Reduce Costs & Improve Outcomes. P&C�Global .�(2025, April 29).�https://www.pandcglobal.com/client-outcomes/major-u-s-health-insurer-uses-analytics-to-reduce-claims-costs-improve-medical-outcomes/�

Verisk. (2023, June 7).�A Surprisingly High Number of Americans Think Insurance Fraud Is Not a Crime, New Survey Shows.�https://www.verisk.com/company/newsroom/a-surprisingly-high-number-of-americans-think-insurance-fraud-is-not-a-crime-new-survey-shows/�

Wells, K. (2025, February 21).�QBE�s profits�surge�in 2024 as underwriting performance tracks ahead of plan. Reinsurance News.�https://www.reinsurancene.ws/qbes-profits-surge-in-2024-as-underwriting-performance-tracks-ahead-of-plan/